Comprehending VA Home Loans: A Comprehensive Guide for Armed Force Families

Wiki Article

Making The Most Of the Conveniences of Home Loans: A Step-by-Step Method to Securing Your Perfect Home

Browsing the complex landscape of home mortgage needs a systematic technique to ensure that you protect the property that straightens with your financial objectives. By beginning with a detailed analysis of your financial setting, you can recognize one of the most ideal financing alternatives available to you. Comprehending the nuances of different financing types and preparing a careful application can dramatically influence your success. However, the details do not finish there; the closing process demands equivalent attention to detail. To truly maximize the advantages of mortgage, one must consider what actions follow this fundamental job.Understanding Home Mortgage Fundamentals

Understanding the principles of home mortgage is essential for anyone considering buying a building. A mortgage, commonly referred to as a home mortgage, is a monetary product that permits people to borrow cash to get realty. The borrower consents to repay the finance over a defined term, generally varying from 15 to thirty years, with passion.

Trick parts of home mortgage include the principal quantity, rate of interest, and payment timetables. The principal is the amount borrowed, while the passion is the expense of borrowing that quantity, shared as a percentage. Rate of interest can be fixed, staying constant throughout the funding term, or variable, fluctuating based on market problems.

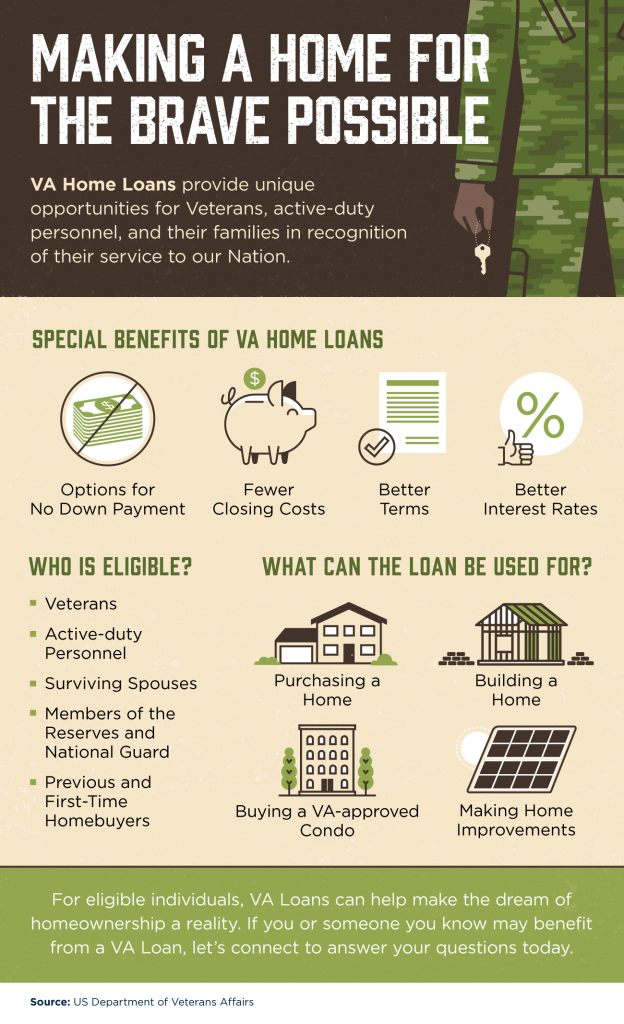

Additionally, debtors should be mindful of various types of home mortgage, such as traditional car loans, FHA fundings, and VA lendings, each with distinct eligibility criteria and benefits. Recognizing terms such as down settlement, loan-to-value ratio, and private home loan insurance coverage (PMI) is also critical for making informed decisions. By realizing these essentials, prospective house owners can navigate the intricacies of the mortgage market and identify choices that straighten with their economic goals and residential or commercial property desires.

Evaluating Your Financial Circumstance

Assessing your financial circumstance is a critical action before beginning on the home-buying trip. Next, checklist all monthly costs, making certain to account for fixed prices like rent, energies, and variable expenditures such as groceries and home entertainment.

After establishing your income and expenses, identify your debt-to-income (DTI) ratio, which is essential for lenders. This ratio is computed by splitting your total monthly debt repayments by your gross regular monthly income. A DTI proportion below 36% is typically taken into consideration beneficial, suggesting that you are not over-leveraged.

Additionally, examine your debt rating, as it plays a critical duty in securing desirable financing terms. A higher credit rating can bring about lower rates of interest, ultimately conserving you money over the life of the financing.

Exploring Loan Choices

With a clear photo of your financial scenario established, the following step involves exploring the various lending choices available to prospective property owners. Comprehending the various sorts of home car loans is crucial in selecting the appropriate one for your needs.Traditional fundings are conventional funding methods that generally need a higher credit report and deposit yet offer competitive rates of interest. On the other hand, government-backed lendings, such as FHA, VA, and USDA lendings, accommodate certain teams and usually need reduced down settlements and credit report, making them available for first-time buyers or those with minimal funds.

One more choice is variable-rate mortgages (ARMs), which include reduced initial prices that readjust after a specified duration, possibly leading to significant financial savings. Fixed-rate home loans, on the other hand, offer stability with a regular rates of interest throughout the financing term, securing you against market Click This Link changes.

Furthermore, think about the financing term, which usually ranges from 15 to thirty years. Much shorter terms may have greater regular monthly payments however can conserve you interest useful content over time. By very carefully assessing these choices, you can make an informed decision that lines up with your monetary goals and homeownership ambitions.

Preparing for the Application

Successfully preparing for the application process is vital for protecting a home financing. A solid debt score is critical, as it affects the lending amount and interest rates readily available to you.Next, gather necessary documentation. Usual requirements include current pay stubs, tax obligation returns, financial institution statements, and evidence of properties. Organizing these documents ahead of time can substantially speed up the application process. In addition, take into consideration getting a pre-approval from loan providers. This not just provides a clear understanding of your borrowing ability yet additionally strengthens your position when making a deal on a building.

Furthermore, establish your budget by considering not just the finance quantity yet likewise property taxes, insurance coverage, and maintenance prices. Finally, familiarize on your own with different funding types and their particular terms, as this knowledge will encourage you to make educated choices throughout the application procedure. By taking these proactive actions, you will certainly boost your preparedness and boost your chances of safeguarding the mortgage that best fits your requirements.

Closing the Deal

Throughout the closing meeting, you will certainly review and sign various papers, such as the funding estimate, shutting disclosure, and home loan agreement. It is essential to thoroughly comprehend these papers, as they outline the car loan terms, payment routine, and closing expenses. Take the time to ask your loan provider or genuine estate agent any kind of concerns you might helpful resources need to avoid misconceptions.

Once all papers are signed and funds are transferred, you will certainly receive the keys to your new home. Keep in mind, shutting prices can differ, so be planned for expenses that may consist of appraisal fees, title insurance policy, and attorney costs - VA Home Loans. By staying organized and informed throughout this process, you can make sure a smooth change right into homeownership, maximizing the benefits of your home financing

Verdict

In final thought, taking full advantage of the advantages of home mortgage demands an organized approach, including a comprehensive evaluation of financial scenarios, exploration of diverse car loan choices, and careful preparation for the application process. By adhering to these actions, possible home owners can boost their chances of securing positive funding and achieving their property ownership objectives. Ultimately, careful navigation of the closing process additionally solidifies a successful change right into homeownership, guaranteeing long-term financial stability and satisfaction.Browsing the facility landscape of home financings requires a systematic approach to guarantee that you secure the home that aligns with your financial goals.Understanding the basics of home loans is vital for any individual thinking about acquiring a residential property - VA Home Loans. A home financing, typically referred to as a home loan, is an economic product that allows individuals to borrow money to get real estate.In addition, debtors should be conscious of different kinds of home finances, such as conventional loans, FHA financings, and VA lendings, each with distinct eligibility requirements and advantages.In conclusion, taking full advantage of the benefits of home financings requires an organized approach, incorporating a comprehensive analysis of economic circumstances, exploration of diverse financing options, and careful preparation for the application procedure

Report this wiki page